SBA Announces New IAL2 Electronic Signature Requirements

Small Business Administration (SBA) lending plays a crucial role in fostering economic growth and supporting aspiring entrepreneurs. In recent years, advancements in digital technologies have transformed the lending process, making it more efficient and accessible. One significant development is the requirement for lenders to use Identity Assurance Level 2 (IAL2) when signing lending forms electronically. This article explores the new requirements issued by SBA and how lenders are using remote closing to provide better, faster, safer service.

New SBA requirements

The SBA announced updated requirements for electronic signatures in SOP 50 10 7, which takes effect August 1, 2023. Like many government agencies, the SBA has embraced the IAL2 standards defined by the National Institute of Standards and Technology (NIST). This heightened level of identity proofing is considered the gold standard for securing sensitive transactions online.

“Modern applications must use technology to validate Applicant data through real time third party databases to protect against fraud, identity theft, and ineligibility. The scale of America’s small business access to capital need calls for solutions resilient enough to support an estimated 33 million small businesses, who compete in a global marketplace that moves at the pace of a click.” - Small Business Administration SOP 50 10 7 Section A, Ch 1

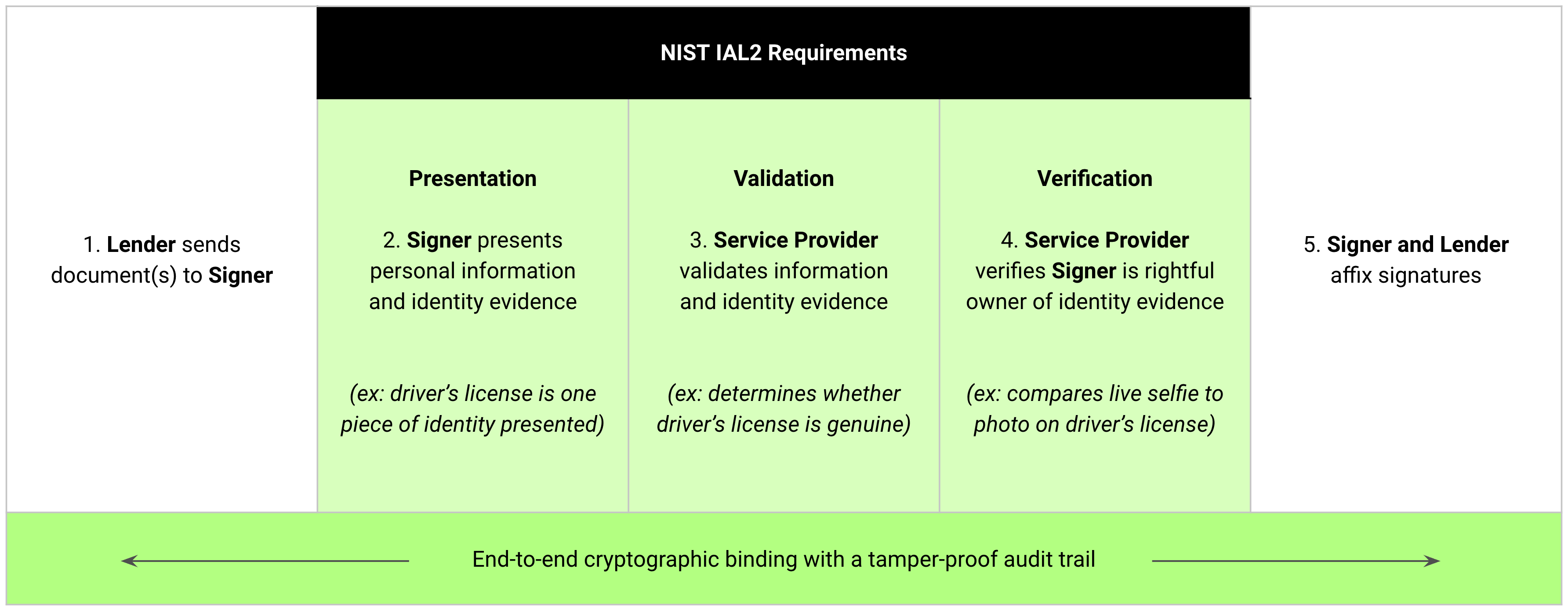

To simplify, IAL2 requires individuals to present personal information and identity evidence. The service provider then validates the accuracy of the information and the genuineness of the evidence and establishes the individual as the true owner of the claimed identity. For example, one of the types of evidence commonly presented is a driver’s license. The service provider validates the authenticity of the driver’s license and verifies that the signer is the rightful owner of that driver’s license, typically by capturing a live selfie which is then compared to the photo on the driver’s license. While not required, best practice is to cryptographically bind each signer’s authenticated identity to the actions they subsequently perform - e.g. data entered, signature applied - in order to produce a tamper proof audit trail.

The new requirements apply to all 7(a) and 504 loans and cover all common document types, including:

- Application Documents

- Loan Closing Documents

- Secondary Market Sale Documents

- Servicing Action

- Liquidation Documents

- Litigation Documents

- Post Default Action Documents

- Delegated Authority Documentation

Advantages of IAL2-Compliant Electronic Signatures

Although meeting the IAL2 standard is a regulatory requirement, it is also a best practice for any kind of transaction that could be challenged in a court of law or where there is the potential for fraud or impersonation. Key advantages include the following:

- Enhanced Security: IAL2 provides an additional layer of protection against identity theft and fraud, instilling confidence in both banks and customers during the lending process. This heightened security is particularly critical for sensitive financial transactions.

- Streamlined Processes: With a digital lending process, the cumbersome paperwork associated with traditional lending is significantly reduced. This streamlined process accelerates loan approval times, enabling banks to serve customers more efficiently.

- Geographical Flexibility: IAL2 allows lenders to authenticate customers remotely, which means they can serve customers anywhere without requiring them to visit a physical branch. This fosters financial inclusion by reaching underserved regions and populations.

- Lower Costs: Digitizing the lending process saves costs associated with physical paperwork, storage, and transportation. These costs routinely add up to several hundred dollars per loan. These cost efficiencies can be passed on to customers through better interest rates or lower fees.

- Tamper-Proof Audit Trail: In any lending agreement it is critical to have strong protections against repudiation. In practice this means capturing a robust audit trail demonstrating that the parties are who they claim to be and the contract was properly and legally executed. This is particularly true for loans that will be sold or securitized as purchasers require strong assurances of the integrity of the loans in the portfolio being acquired.

About Proof

Proof makes it easy for lenders to meet the new SBA requirements. We are the only IAL2-compliant eSign provider with a secure, flexible platform that can be up-and-running in less than a day. We’re proud to be trusted by 5 of the 10 top largest US banks and a fast-growing community of innovative lenders.

.jpg)

.png)