The Leading Platform for Secure Financial Document Signing

Financial documents authorize real money moving in real time. A forged signature, a tampered record, or an impersonated customer can result in losses that no workflow tool will recover.

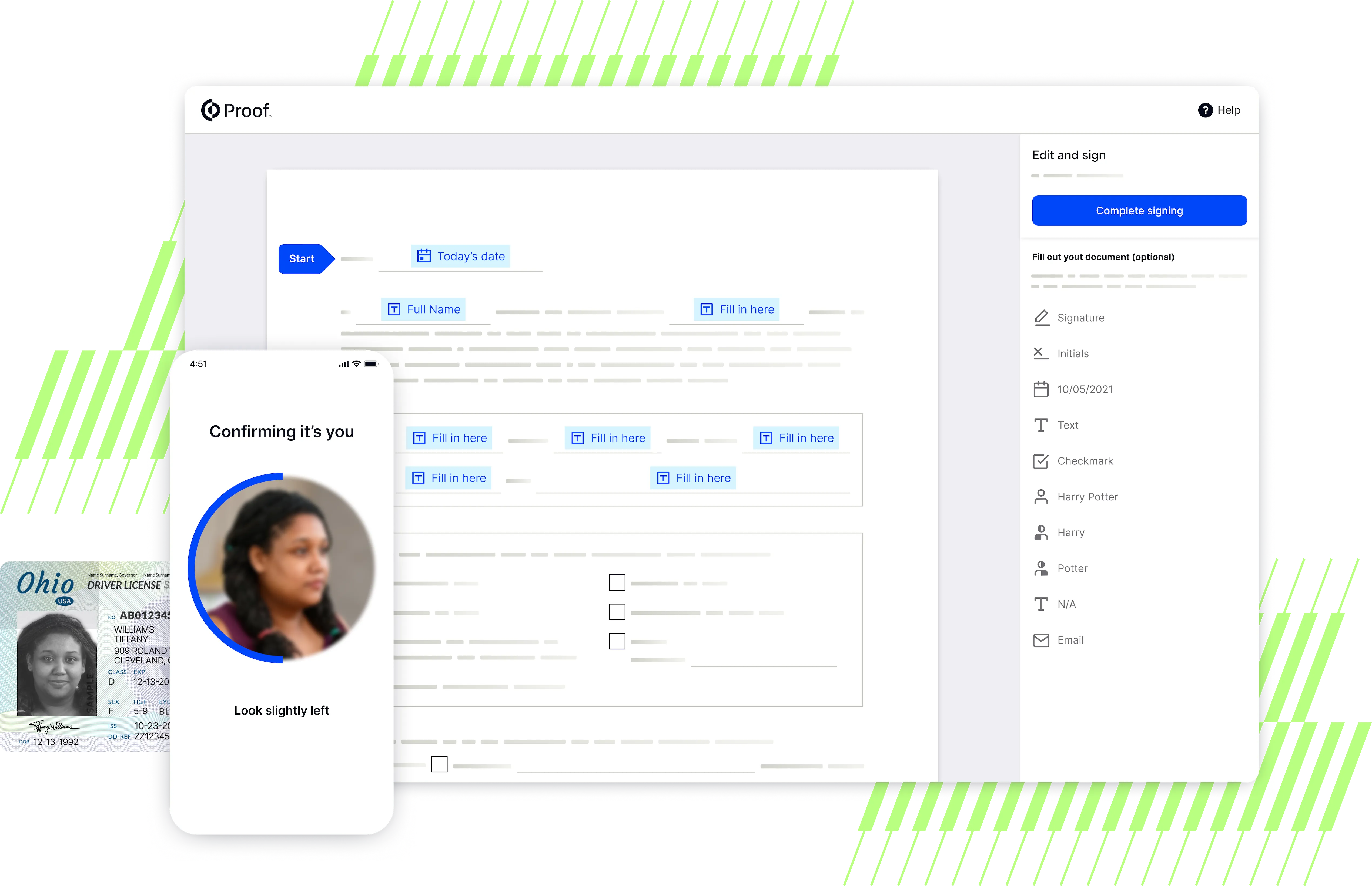

Proof treats signing as an identity event, not just a paperwork step.

What makes financial document signing different

Signing a wire authorization is not the same risk profile as signing a sales contract. Financial documents carry immediate legal and financial weight. They get disputed, surface in audits, become evidence.

Standard e-signature platforms capture consent. For financial services, you need to prove the right person signed and that no one altered the document afterward. That requires a different class of platform.

What to look for

Identity verification tied to the signature

Confirm signers at IAL2 — government ID, biometric match, liveness detection. Email auth and knowledge-based questions can be guessed.

Cryptographic record integrity

The signed document must be cryptographically sealed. Any modification after signing should be immediately detectable.

Forgery and fraud detection

Active monitoring at signing— credentials, behavioral signals, network patterns — catches fraud before it completes, not after

Audit trail that stands on its own

A tamper-evident log of who signed, when, and how— producible without a vendor certification letter.

Regulatory compliance

SOC 2, WebTrust, ESIGN, and UETA are baseline. Financial institutions should also verify FINRA and SEC compliance.

Notarization support

The platform should handle notarization natively, not route to a third party. A disconnected workflow breaks chain of custody.

How platforms compare

Feature | Proof Sign | General-purpose eSign | PKI-based signing tools |

|---|---|---|---|

IAL2 identity verification | Add-on | — | |

Cryptographic document binding | Partial | Not included | |

Active fraud /deepfake detection | — | — | |

Notarization (RON) | — | — | |

Tamper-evident audit trail | |||

WebTrust audited | — | — | |

Best for | High-stakes financial workflows | Standard business contracts | PDF compliance workflows |

Committed to the highest standards

Proof adheres to strict security standards and regulations thoroughly validated by third-party assessors. We are committed to the protection of customer data and accessibility.

Frequently Asked Questions

Is an e-signature legally binding for financial documents?

Yes, under ESIGN and UETA, e-signatures are legally binding for most financial documents. The risk is not legal validity —it's proving who signed if the transaction is disputed. That's where identity verification tied to the signature becomes critical.

What's the difference between an e-signature and a digital signature for financial documents?

An e-signature captures intent. A digital signature cryptographically seals the document and binds the signature to the signer's verified identity. For documents where authenticity may be challenged, digital signatures with identity verification provide significantly stronger protection.

Can Proof handle notarized financial documents?

Yes. Proof's Notarize product supports documents requiring notarization —including financial affidavits, powers of attorney, and loan documents — through an online notarization workflow accepted in all 50 states.