The Best eClosing Platform

The right eClosing platform determines which closing options are available for every transaction, integrates with your existing systems, and protects against the fraud that targets real estate more than almost any other industry.

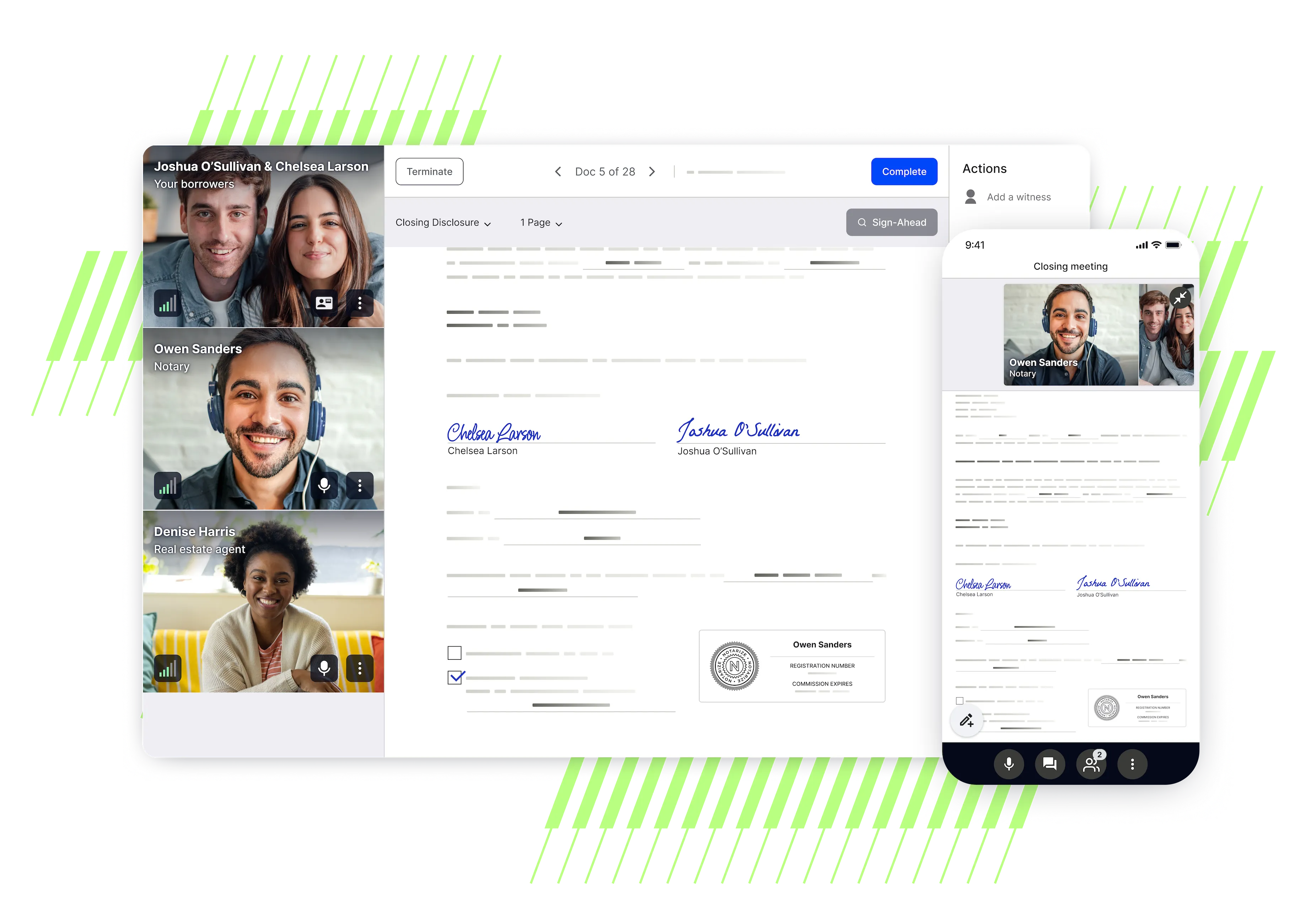

That’s Proof.

The industry is moving to digital closing — and borrowers expect it

90% of mortgage lenders now offer digital closings, and 88% of borrowers say they want a fully digital process.

Title agencies and lenders are now focused on scaling digital closings across more transaction types, more states, and more of their loan portfolio.

Driving Adoption of Remote Online Notarization and Digital Real Estate Transactions

Remote Online Notarization (RON) in 2026: What Every Title Professional Needs to Know

What to look for

Eligibility intelligence

Closing eligibility depends on loan type, county, underwriter requirements, and RON laws. The best platforms automate this determination for every transaction.

Integration with your existing stack

A platform that doesn't connect to your LOS and title software creates manual work that negates efficiency gains. Look for integrations that are live and documented.

Fraud protection built into the closing

Seller impersonation is the fastest-growing real estate fraud vector. Identity verification at the point of signing, rather than at file opening, is what stops it.

Support for both hybrid and full eClosings

Some transactions qualify for full RON, others require a hybrid approach. The right platform handles the full spectrum in a single workflow.

MISMO certification

A meaningful signal for enterprise-grade platforms,reflecting independent validation against mortgage industry standards.

Signer experience and accessibility

Signers should complete from any device without downloads. Closing abandonment from poor UX is a real cost, especially for cash sales and unfamiliar signers.

How platforms compare

Feature | Proof Sign | General-purpose eSign | PKI-based signing tools |

|---|---|---|---|

Full eClosing (RON) | Partial | ||

Hybrid closing | |||

Automatic eligibility determination | (4.5M rules) | — | — |

Built-in fraud / ID verification | — | — | |

LOS integrations (Encompass, etc.) | Partial | ||

MISMO certified | — | — | |

Best for | Full-spectrum eClosing at scale | High-volume hybrid workflows | Flexible RON closings |

Committed to the highest standards

Proof adheres to strict security standards and regulations thoroughly validated by third-party assessors. We are committed to the protection of customer data and accessibility.

Frequently Asked Questions

What's the difference between a hybrid closing and a full eClosing?

A hybrid closing signs some documents electronically and others in person. A full eClosing completes the entire package online, including notarized documents through RON. Proof supports both and determines the best option for each transaction based on eligibility rules.

How does digital closing protect against fraud?

Proof verifies signer identity before they can access closing documents — using biometric matching, government ID analysis, and liveness detection. This stops seller impersonation, one of the fastest-growing fraud types in real estate.

How long does it take to implement a digital closing platform?

Most title agencies and lenders are up and running on Proof in under a week. Proof fits into existing systems and doesn't require replacing your loan origination system or title production software.