The Benefits of A Digital Real Estate Closing

The traditional closing table costs title agents an average of 157 minutes per transaction and introduces error rates that delay funding and frustrate buyers.

Digital real estate closings (whether hybrid or fully online) change both of those numbers significantly.

The industry is moving to digital closing — and borrowers expect it

90% of mortgage lenders now offer digital closings, and 88% of borrowers say they want a fully digital process.

Title agencies and lenders are now focused on scaling digital closings across more transaction types, more states, and more of their loan portfolio.

Driving Adoption of Remote Online Notarization and Digital Real Estate Transactions

Remote Online Notarization (RON) in 2026: What Every Title Professional Needs to Know

The measurable benefits

Faster closings

Title agents save 157 minutes per closing. Lenders cut up to 7 days from the funding cycle, gains that compound across thousands of transactions.

Fewer errors

Digital workflows reduce closing package error rates by 31%. They eliminate the whole category of errors that come from unguided paper signing.

Lower cost per closing

Full eClosings save an average of $443 per home loan, including reduced courier costs, fewer re-draws, and faster funding.

Convenient for buyers and sellers

Signers complete from anywhere, at any time. For relocation and investor closings, this removes a significant friction point.

Built-in fraud protection

Proof verifies signer identity using biometric matching and behavioral signals, stopping seller impersonation fraud before it happens.

Defensible records

Every digital closing produces a tamper-evident audit trail, ready if a transaction is disputed or a regulator asks.

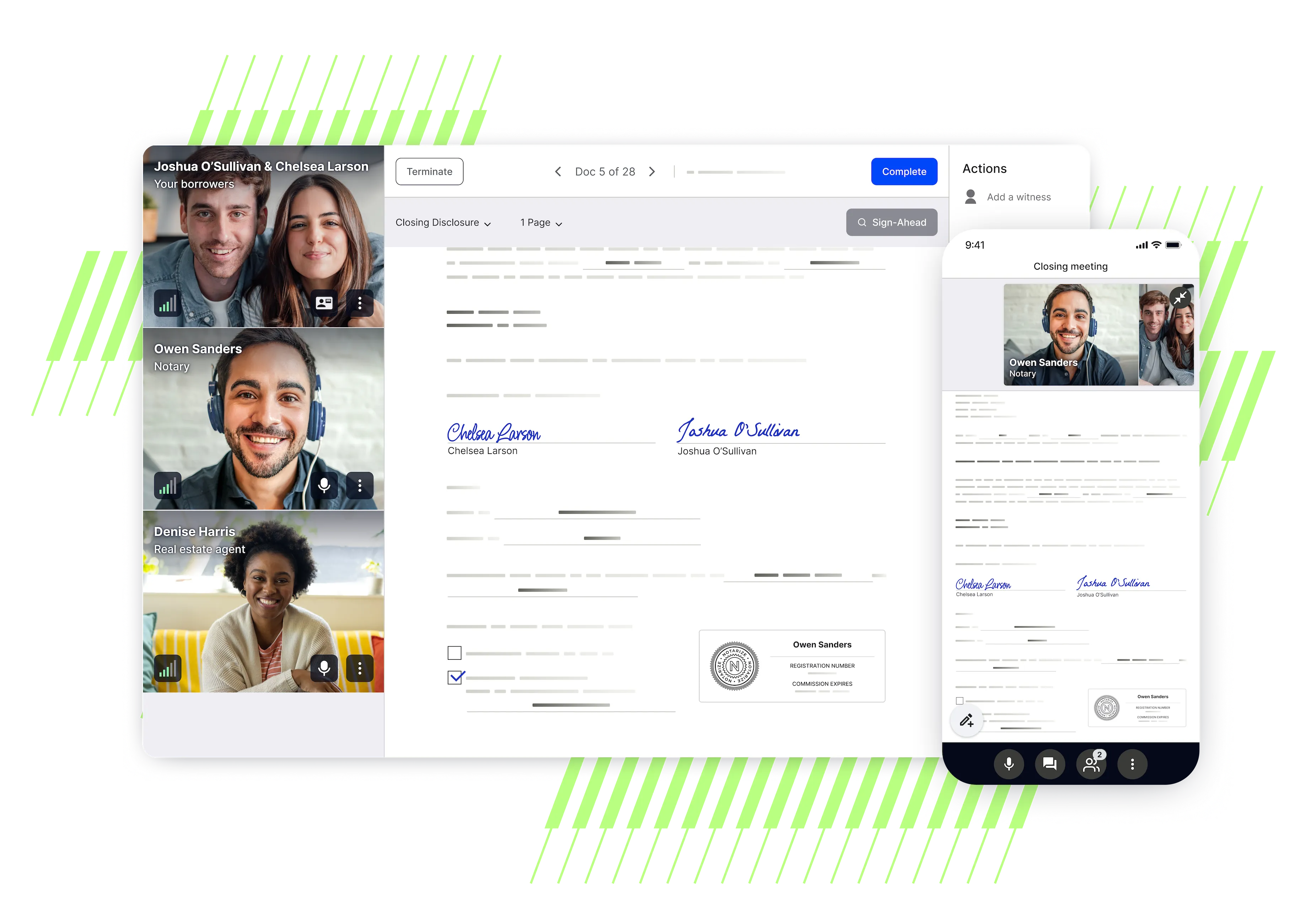

Closing with Proof

Proof supports the full spectrum of closing types:

✔️ Hybrid eClosings

✔️ Full RON eClosings

✔️ HELOCs

✔️ Loan modifications

The Proof Engine® references 4.5 million closing eligibility rules to determine the best option for every transaction automatically. That means no guesswork about what a given county, underwriter, or loan type will accept.

Plus, Proof integrates with the systems title agencies and lenders already use: Encompass by ICE Mortgage Technology, SoftPro, Resware, DocMagic, and others.

Over $640 billion in real estate transactions have been secured through the Proof platform.

We've spent more than a decade making Proof the easiest, most secure, and most trusted way to close.

Committed to the highest standards

Proof adheres to strict security standards and regulations thoroughly validated by third-party assessors. We are committed to the protection of customer data and accessibility.

Frequently Asked Questions

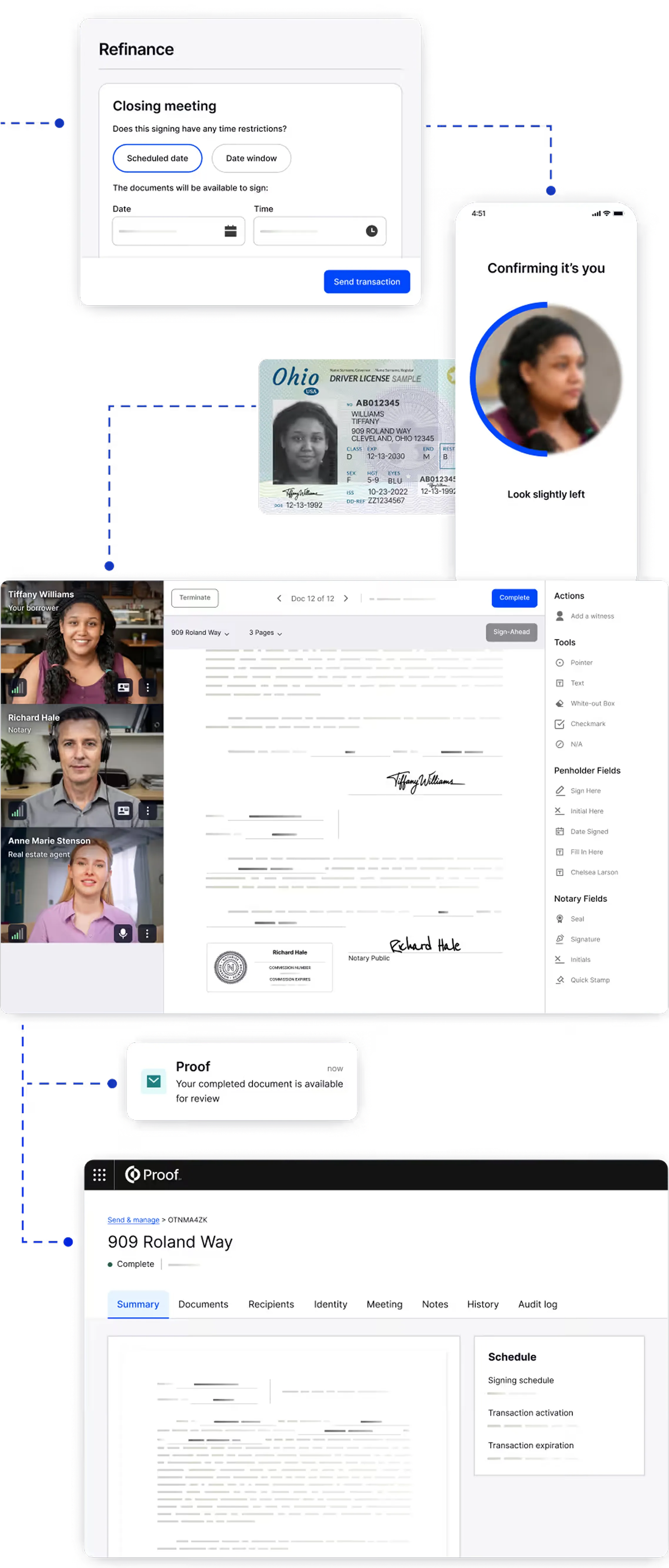

What's the difference between a hybrid closing and a full eClosing?

A hybrid closing signs some documents electronically and others in person. A full eClosing completes the entire package online, including notarized documents through RON. Proof supports both and determines the best option for each transaction based on eligibility rules.

How does digital closing protect against fraud?

Proof verifies signer identity before they can access closing documents — using biometric matching, government ID analysis, and liveness detection. This stops seller impersonation, one of the fastest-growing fraud types in real estate.

How long does it take to implement a digital closing platform?

Most title agencies and lenders are up and running on Proof in under a week. Proof fits into existing systems and doesn't require replacing your loan origination system or title production software.